Medicare Supplement Insurance (also called Medigap) is a type of private insurance plan that can work alongside your Original Medicare coverage to help cover some out-of-pocket Medicare costs such as copayments, coinsurance and deductibles.

You can compare different types of Medicare plans, including Medicare Supplement Insurance, to find the type of coverage that's the best fit for your needs.

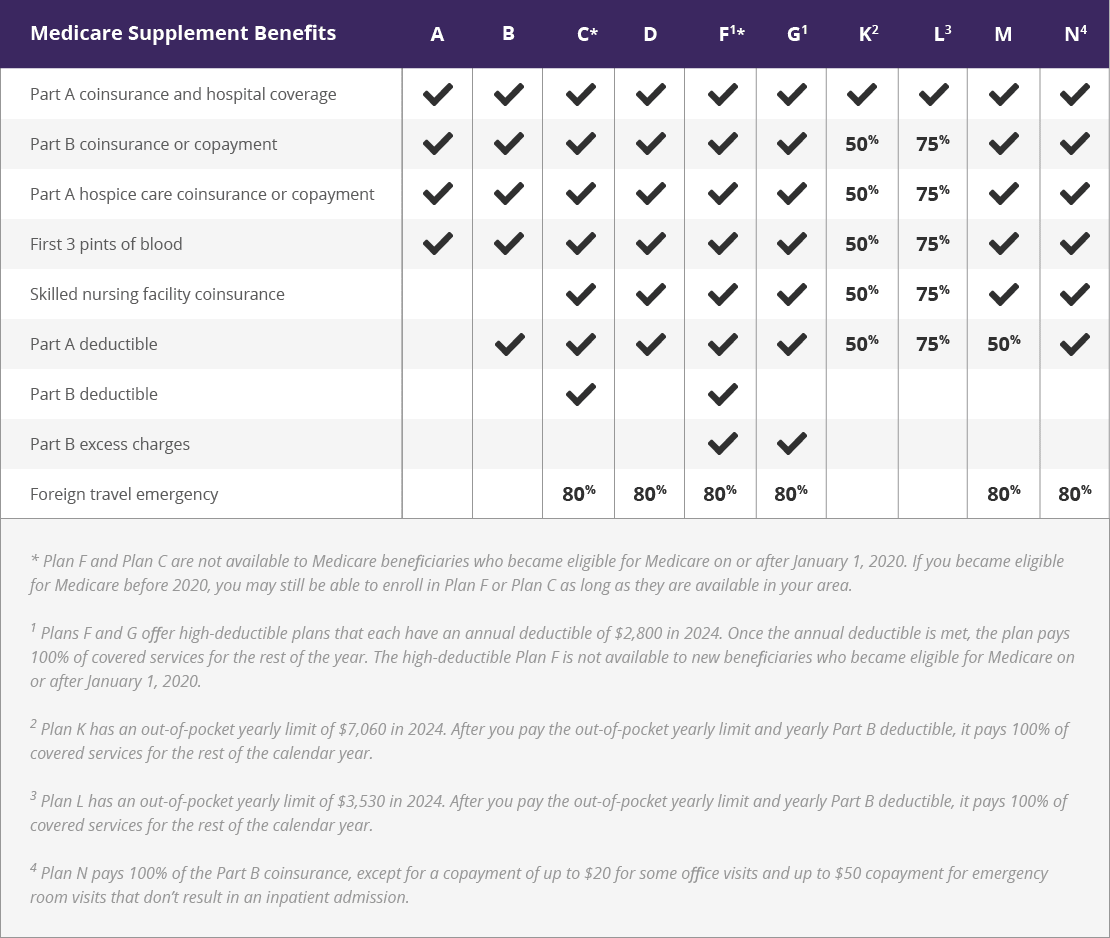

How does Medicare Supplement Insurance work?

After you enroll in Original Medicare (Medicare Part A and Part B), you may incur some out-of-pocket Medicare costs when you use your coverage.

For example, you have to meet the Medicare Part B deductible ($283 in 2026) before Part B will start covering some of the costs of your care. And once it does, you are still typically responsible for a 20 percent Part B coinsurance for approved services.

A Medicare Supplement Insurance plan can help provide coverage for some of these out-of-pocket Medicare costs.

You typically pay a monthly premium to belong to a Medigap plan.

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

| Part B coinsurance or copayment |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

50% |

75% |

✓ |

✓ |

| Part A hospice care coinsurance or copayment |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

50% |

75% |

✓ |

✓ |

| First 3 pints of blood |

✓ |

✓ |

✓ |

✓ |

✓ |

✓ |

50% |

75% |

✓ |

✓ |

| Skilled nursing facility coinsurance |

|

|

✓ |

✓ |

✓ |

✓ |

50% |

75% |

✓ |

✓ |

| Part A deductible |

|

✓ |

✓ |

✓ |

✓ |

✓ |

50% |

75% |

50% |

✓ |

| Part B deductible |

|

|

✓ |

|

✓ |

|

|

|

|

|

| Part B excess charges |

|

|

|

|

✓ |

✓ |

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

What can Medicare Supplement Insurance plans cover?

Medicare Supplement Insurance can provide coverage for some or all of the following costs:

There are 10 Medicare Supplement Insurance plans available in most states. They are designated a plan letter (Medigap Plan A, B, C, D, F, G, K, L, M and N), and each type of plan offers a different combination of some or all of the above coverage.

Not every plan will be available in every state.

Learn more about Medigap plans in your area

Speak with a licensed insurance agent

What does Medicare Supplement Insurance cost?

Medicare Supplement Insurance is sold by private insurance companies, so the cost of a plan can differ between one carrier or location and another.

There are a few other things that may affect the cost of a Medigap plan:

- The amount of coverage offered by the plan

- Whether or not medical underwriting is used as part of the application process

- The age at which you join the plan

- Eligibility for any discounts offered by the carrier

- Gender (women often pay less for a plan than men)

Medigap eligibility

In order to be eligible for a Medicare Supplement Insurance plan, you must be at least 65 years old, enrolled in Medicare Part A and Part B and reside in the area that is serviced by the plan.

Some states – but not all – allow Medicare Supplement Insurance enrollment for Medicare beneficiaries under the age of 65.

The following states require insurance companies to offer at least one Medicare Supplement plan to Medicare beneficiaries under 65:

- California, Colorado, Connecticut, Delaware, Florida, Georgia, Hawaii, Illinois, Kansas, Louisiana, Maine, Maryland, Massachusetts, Michigan, Minnesota, Mississippi, Missouri, New Hampshire, New Jersey, New Mexico, New York, North Carolina, Oklahoma, Oregon, Pennsylvania, South Dakota, Tennessee, Texas, Vermont and Wisconsin.

If you are currently enrolled in a Medicare Advantage (Part C) plan, you will not be eligible to sign up for a Medicare Supplement Insurance plan. You must disenroll from your Medicare Advantage plan before you can join a Medigap plan.

Enrolling in a Medigap plan

Your six-month Medigap Open Enrollment Period begins when you are 65 years old and enrolled in Part A and Part B.

During your Medigap Open Enrollment Period, insurance companies are not allowed to use medical underwriting to determine your premium rates when you apply for a policy. This means that if you apply for a plan during this period, you cannot be charged more due to your age or health history.

Once your six-month open enrollment window ends, you may be subject to underwriting and may pay higher plan premiums. Insurance companies also reserve the right to deny you a policy based on the results of the underwriting. That’s why it’s highly advisable to take advantage of your Medigap open enrollment period.

There are some special enrollment periods for Medicare Supplement Insurance that give you guaranteed issue rights, which means insurance companies can't use underwriting in your application process. You have to meet specific criteria to qualify for one of these special enrollment periods.

If one of the following situations applies to you, you may qualify for a Medigap special enrollment period:

- You received a Medicare Supplement Insurance plan through your employer, and that coverage ended.

- You belong to a Medicare Advantage plan, and the plan stops serving your area or you move out of the plan’s service area.

- You have a Medicare SELECT plan, and you move out of the plan’s service area.

- You joined a Medicare Advantage plan or PACE when you first became eligible, and you decided to leave the plan within one year of enrolling.

- You dropped a Medigap plan in favor of a Medicare Advantage or Medicare SELECT plan, and you wish to switch back to a Medigap plan within one year.

- You are enrolled in a Medigap plan, and the plan ends through no fault of your own.

- You are enrolled in a Medicare Advantage or Medigap plan provided by a company that misled you or was found to have not followed certain regulatory rules.

Frequently asked questions about Medicare Supplement Insurance

What is the difference between Medicare Supplement and Medicare Advantage?

Medicare Supplement plans and Medicare Advantage plans work very differently, and you can't have both at the same time.

Medicare Supplement plans work alongside your Original Medicare coverage to help cover out-of-pocket Medicare costs like deductibles and coinsurance.

Medicare Advantage plans replace your Original Medicare coverage. Plans can also offer other benefits Original Medicare doesn't typically cover.

Learn more about the differences between Medigap and Medicare Advantage

What are the rates for different Medicare Supplement plans?

Medicare Supplement plan premiums can vary based on where you live, the insurance companies offering plans, the pricing structure those companies use and the type of plan you apply for.

Learn more about Medigap rates and how to compare plan costs

What should I look for in a Medicare Supplement plan?

With 10 different types of standardized Medigap plans and a range of benefits they can offer (not to mention the range of monthly premiums for each plan), it can be helpful to take the time to compare the Medigap options available where you live.

Learn more about the benefits, coverage, and costs to consider when comparing Medigap plans

When can I change my Medicare Supplement plan?

You can usually change your Medicare Supplement plan at any time during the year. You should consider switching Medigap plans during certain times of the year, however.

Changing Medicare Supplement plans during the right time can help protect you from having to pay higher premiums or being denied coverage due to your health or preexisting conditions.

Learn more about when to change your Medicare Supplement plan

How are Medicare Supplement providers rated?

There are a number of different Medicare Supplement Insurance companies across the nation. The companies that sell Medigap plans in your area may vary. You can learn more about them by comparing company ratings and reading customer reviews.

Learn more about some of the top Medicare Supplement Insurance companies

Why is Plan F popular?

Medigap Plan F covers more out-of-pocket Medicare costs than any other standardized type of Medigap plan. In exchange for their monthly premium, Plan F beneficiaries know that all of their Medicare deductibles, coinsurance, copays and other out-of-pocket costs will be covered.

For many Medicare Supplement beneficiaries, this piece of mind and ease of use are the reasons they chose to enroll in Plan F.

Learn more about Plan F and see customer reviews

Learn about the average cost of Plan F

How did Medicare Supplement plans change in 2020?

New Medicare beneficiaries who first became eligible for Medicare on or after January 1, 2020 are no longer able to enroll in Medigap Plan F or Plan C.

If you already had Plan F or Plan C, you can keep your plan. If you became eligible for Medicare before Jan. 1, 2020, you can apply for Plan F or Plan C if either plan is available where you live.

Also introduced in 2020 was a high-deductible Plan G, which offers comparatively lower monthly premiums in exchange for having to meet an annual deductible before Plan G benefits kick in.

Learn more about Plan F, Plan N and Plan G in 2026.

Learn more about Medigap plans in your area

Speak with a licensed insurance agent

{kind=link}