The average cost of a Medicare Supplement Insurance plan was $150 per month in 2024.1 But the average cost of each type of Medicare Supplement (also called Medigap) plan can vary quite a bit from one plan type to another.

Factors such as age, gender, smoking status, health and where you live can also affect Medicare Supplement plan rates.

Some insurance companies offer discounts that can lower Medicare Supplement plan premiums.

Compare Medicare Supplement plan rates available where you live.

Speak with a licensed insurance agent

How much does each Medigap plan cost?

The chart below shows the average monthly premium for each the most popular types of Medicare Supplement Insurance plans in 2024.1

It's important to note that premiums may be different where you live, and some types of Medigap plans have far fewer enrollees than other types of plans in certain geographic areas. This difference in enrollment can affect the monthly premium that is paid by Medigap beneficiaries.

2024 Average Monthly Medicare Supplement Premiums

| Medicare Supplement Insurance Plan |

2024 Average monthly premium |

| F* |

$223.89 |

| G |

$154.99 |

| High Deductible G |

$58.09 |

| N |

$127.27 |

*Plan F is only available to beneficiaries who first became eligible for Medicare before January 1, 2020. If you were eligible for Medicare before that date or already have Plan F, you may be able to stay enrolled or sign up for a new Plan F if it's available where you live

How much will Medicare Supplement Insurance cost in my state?

Because Medicare Supplement Insurance plans are sold by private insurance companies, plan rates will vary from one market to the next.

In 2024, the average monthly premium rate of Medicare Supplement Plan G in New York was $400 per month. In the same year, the average monthly cost of Medigap Plan G in Iowa was $130.1

The difference in Medigap rates from one state to another can vary widely, similar to how the cost of a gallon of gas can differ greatly from one state to another.

Medigap rates can vary based on carrier

Original Medicare (Part A and Part B) premiums are standardized by the federal government. Private insurance companies that offer Medicare Supplement Insurance plans, however, are free to set their own rates.

How a carrier rates (prices) its plans, inflation and other factors can cause premiums to change over time.

Certain Medigap plans that offer more benefits may cost more

Each type of Medicare Supplement Insurance plan offers a different combination of benefits standardized by the federal government. This means that rates may vary depending on the Medigap plan type.

Generally speaking, plans that offer more standardized benefits may cost more than plans with fewer benefits.

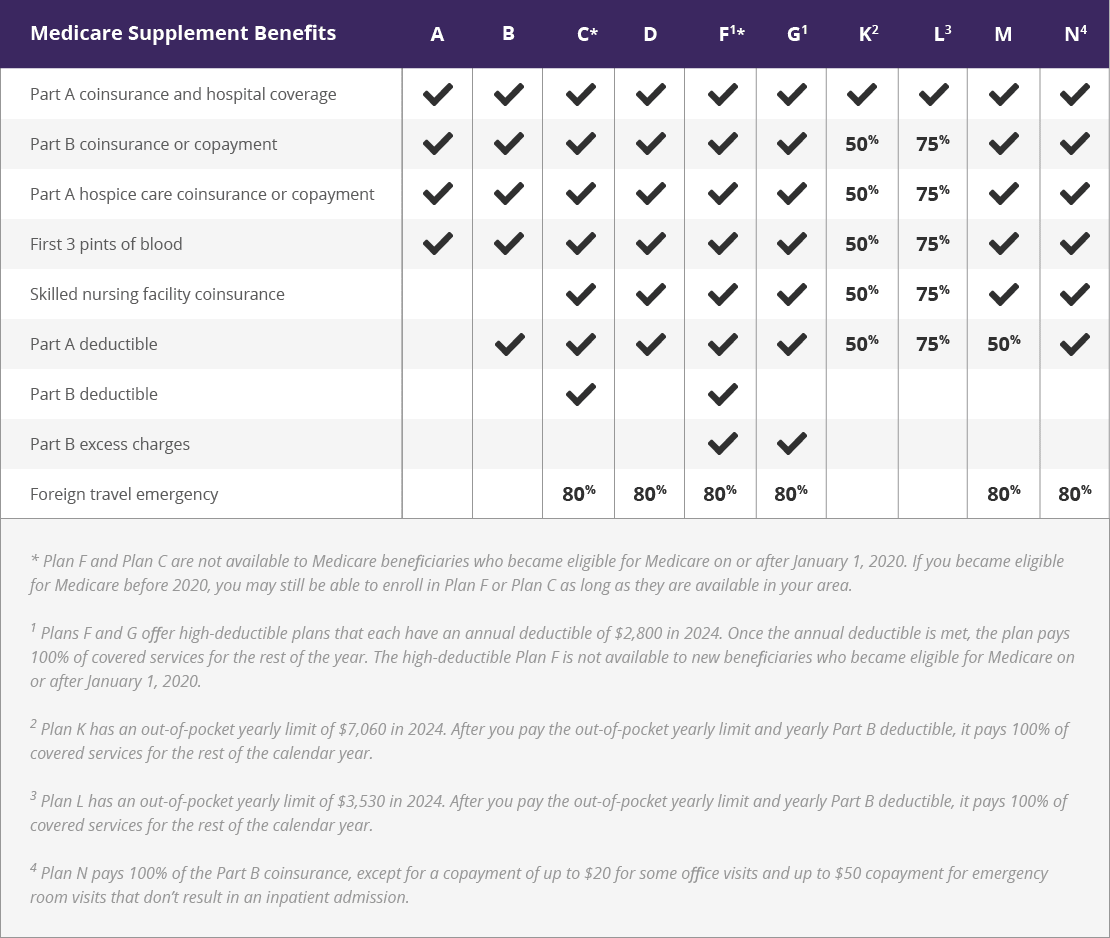

The chart below can help you compare Medigap plans in 2025. (Note: Medigap plans are standardized differently in Massachusetts, Minnesota and Wisconsin.)

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

|

|

|

|

|

|

|

|

|

|

| Part B coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A hospice care coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| First 3 pints of blood |

|

|

|

|

|

|

50% |

75% |

|

|

| Skilled nursing facility coinsurance |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A deductible |

|

|

|

|

|

|

50% |

75% |

50% |

|

| Part B deductible |

|

|

|

|

|

|

|

|

|

|

| Part B excess charges |

|

|

|

|

|

|

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

Medical underwriting could affect your Medigap plan rates

If you apply for a Medicare Supplement Insurance plan after your six-month Medigap Open Enrollment Period (OEP), you may be subject to medical underwriting.

- Your Medigap Open Enrollment Period starts as soon as you are at least 65 years old and enrolled in Medicare Part B.

- During the six months of your Medigap OEP, insurance companies cannot deny you a Medigap plan or charge you higher plan premiums based on your health.

But outside of your Medigap OEP, an insurance company reserves the right to determine your Medigap rates based on your health — unless you qualify for a guaranteed issue right.

Beneficiaries with certain health conditions might face higher rates because they are deemed to be riskier to insure, or they may be denied a Medigap plan altogether.

Insurance companies use different pricing structures to determine rates

There are three different pricing models that insurance companies can use to determine how your Medicare Supplement Insurance plan rates may increase in the future.

Each type of pricing system can produce a different rate for current and incoming plan members.

- Community-rated plans charge the same rate for every plan member, regardless of age. For example, a 75-year-old Medigap beneficiary with a community-rated plan will pay the same rate as a 65-year-old beneficiary with the same plan.

- Issue-age-rated plans have rates based on the age at which you purchased the plan. Your premium rate will be fixed and it won’t change as you age. While your initial Medigap rate could be higher than a community-rated plan, it could potentially cost less in the long term.

- Attained-age-rated plans have rates that increase as you age. As you get older, your Medigap rate will gradually go up.

Some insurance companies may offer Medigap plan discounts for women, non-smokers, married couples, those who pay their premium for the entire year and more.

Be sure to ask your plan provider if they offer any discounts before you sign up for a Medigap plan.

Medigap premiums may increase over time due to other factors, such as inflation.

Compare Medicare Supplement rates in your area

A licensed insurance agent can help you compare the Medicare Supplement Insurance plans that are available where you live, including the plan rates.

Compare Medicare Supplement plan rates available where you live.

Speak with a licensed insurance agent

{kind=link}