This guide explains 2026 Medicare Open Enrollment and other Medicare enrollment periods. Don't miss this important time to review and change your Medicare coverage.

Read moreSpeak with a licensed insurance agent

Speak with a licensed insurance agent

Compare plans today.

Medicare Part D plans provide prescription drug coverage for Medicare enrollees. Part D plans are offered by private insurance companies, not the federal government.

Medicare prescription drug coverage is typically offered through the following types of Medicare plans:

Medicare Part D provides prescription drug coverage for Medicare enrollees. Part D plans are offered by private insurers, not the federal government.

Each Part D prescription drug plan may have varying benefits, costs and rules.

We offer plans from Humana, UnitedHealthcare®, Anthem Blue Cross and Blue Shield*, Aetna, HealthSpringSM, Wellcare, or Kaiser Permanente.

Enrollment may be limited to certain times of the year. See why you may be able to enroll today.

By clicking "Sign me up!” you are agreeing to receive emails from MedicareAdvantage.com. Your Medicare guide will arrive in your email inbox shortly. You can also look forward to informative email updates about Medicare and Medicare Advantage. If you'd like to speak with an agent right away, we're standing by for that as well. Give us a call! LICENSED AGENTS AVAILABLE NOW

Thanks for signing up for our emails!

To compare Medicare Advantage Prescription Drug plans where you live, you can call to speak with a licensed insurance agent. You can also compare plans online for free.

Enrollment may be limited to certain times of the year. See why you may be able to enroll.

You can also compare Part D plans online when you visit MyRxPlans.com.

| Enrollment period | Dates | What you can do during this period |

|---|---|---|

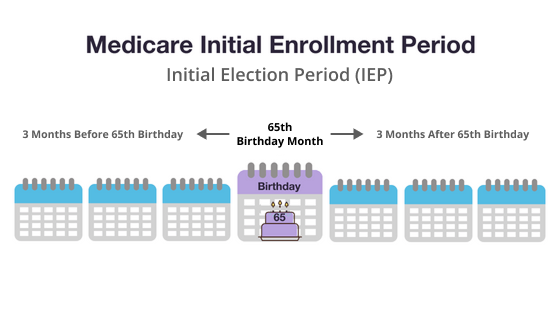

| Initial Enrollment Period (IEP) | Starts 3 months before the month you turn 65 Ends 3 months after the month you turn 65 |

- Sign up for a Medicare Part D plan |

| Medicare Open Enrollment Period (aka the Annual Enrollment Period, or AEP) | Starts October 15 Ends December 7 |

- Sign up for a Medicare Part D plan - Switch Medicare Part D plans - Leave a Medicare Part D plan |

| Special Enrollment Period (SEP) | Depends on your personal situation. See more information below. | - Depends on your personal situation |

You must wait for a qualifying enrollment period to sign up for, make changes to, or leave a Medicare Part D plan.

You can join a Medicare prescription drug plan during your Initial Enrollment Period (IEP).

Your IEP is 7 months long. It starts 3 full months before the month you turn 65. It continues through the month of your 65th birthday, and then for another 3 full months.

Example: You turn 65 on June 5. Your IEP starts on March 1 (3 full months before June) and ends September 30 (3 full months after June).

If you are enrolling during your IEP, your coverage will start at the following times:

You can enroll in a Medicare prescription drug plan between April 1 and June 30.

You can enroll in a Medicare prescription drug plan after you have been getting Social Security or Railroad Retirement Board benefits for 21 full months. After that point, you have 7 full months to enroll in a Medicare prescription drug plan.

You can make changes to your current Part D plan, switch plans, or drop your prescription drug coverage entirely during the annual fall Medicare Open Enrollment Period, which runs from October 15 to December 7 each year.

Also called the Annual Enrollment Period (AEP) or the Annual Election Period, this period takes place every year between October 15 and December 7.

During AEP, you may:

If you make changes during this time, your new coverage will begin on January 1 of the following year.

A Special Enrollment Period (SEP) may be granted for people who have specific qualifying circumstances.

These qualifying situations include, but are not limited to:

A licensed insurance agent can help you find out if you qualify for a Special Enrollment Period. Depending on your qualifying circumstance, you may or may not be eligible to enroll in a Part D plan a certain Special Enrollment Period.

Are you looking to enroll in a Medicare Part D prescription drug plan?

To compare plans where you live, you can call to speak with a licensed insurance agent. You can also compare plans online for free when you visit MyRxPlans.com.

Eligible Medicare beneficiaries can only enroll in Medicare prescription drug coverage during predetermined enrollment periods unless they have a Special Enrollment Period due to a qualifying life event.

Part D plans have different formularies, tiers, coverage rules, and pharmacy networks.

Coverage rules such as quantity limits, prior authorization and step therapy may limit how and when you receive your prescription drugs.

Part D plans also can have pharmacy networks, which may impact the cost of your prescription drugs.

Medicare Part D prescription drug plans don't pay for everything.

If you have a Part D plan, you may have to pay premiums and other out-of-pocket costs like deductibles and copayments.

Medicare Part D plan beneficiaries will have their out-of-pocket costs capped at $2,000 for covered drugs in 2025.

Beneficiaries who do not enroll in a plan that includes Part D coverage when they are first eligible, may face an additional late enrollment penalty (LEP). This additional charge will be applied to the premium and be in place for the duration of their plan enrollment.

You can compare Medicare Part D plans and Medicare Advantage Prescription Drug plans online or call to speak with a licensed insurance agent to get help comparing plans available where you live.

There are many Part D plans to choose from. There are 464 2025 Part D plans offered nationwide.1

A Medicare formulary is the list of prescription drugs that are covered by a particular Medicare Part D or Medicare Advantage plan.

Each plan includes its own formulary that determines which drugs are covered by the plan and how much the drugs cost based on which tier the drug is classified into.

Drugs on a Medicare formulary are divided into tiers that determine the cost paid by beneficiaries.

For example, a tier 1 drug might consist of low-cost, generic drugs and require only a small copayment in order to fill a prescription. A tier 4 drug, however, might be a more expensive name brand drug that requires a higher copayment.

The number of drug tiers and the cost breakdown will vary according to each plan.

Drugs may be added or removed from the market at any time, and therefore drugs may be added or removed from a plan’s formulary. Drugs may also remain for sale on the market but be removed from a plan’s formulary for a variety of reasons.

Beneficiaries reserve the right to request that a Medicare plan cover a particular drug. You can also request to pay a lower amount for a covered drug.

All Medicare formularies generally must include coverage for at least two different drugs within most drug categories, and they must include all available drugs for the following categories:

A Medicare formulary won’t include over-the-counter drugs or weight-loss drugs.

Some drugs on a Medicare formulary come with certain types of restrictions, such as:

Of course, your current list of prescription medications is a great place to start in understanding how extensive you need your Part D plan to be.

Make a list of every prescription drug you currently take and make note of whether or not the prescription is a brand name or generic option.

Check this list against the covered drug lists of the Part D plans you are evaluating.

It’s important to take a look at all the copays and costs for drugs that you are currently taking so that you get a sense of what the plan AND the costs of your regular medications will cost each year.

It is also important to note that no plan covers every single drug and copays may vary. You may be able to find lower out-of-pocket costs at specific pharmacies, depending on the plan.

If this is your first time enrolling in Part D, you may be surprised by some of the variability in plans that you may experience each year.

There are a few major things that can change from year to year:

This is why it’s important to check your Part D plan coverage every year.

Make sure you compare your current list of brand and generic prescription drugs against your plan’s new formulary and cost breakdown to see if you are still appropriately covered.

If you need prescription drug coverage, it is important to enroll in a Part D plan during your Initial Enrollment Period or when you are first eligible for Part D coverage. If not, you may face a late enrollment penalty which will be in force for the duration of your plan enrollment.

If your IEP ends and there is a period of 63 days or more in a row when you do not have creditable prescription drug coverage, you may have a late enrollment penalty added to your monthly premium for as long as you have Medicare prescription drug coverage.

|

Creditable coverage includes a Medicare Part D plan, a Medicare Advantage plan or a Medicare health plan that offers drug coverage, or other drug coverage that pays at least as much as Medicare's standard prescription drug coverage. The amount you pay for the Part D late enrollment penalty depends on how long you went without creditable drug coverage. |

Drug coverage is creditable if it pays – on average – at least as much as the standard Medicare prescription drug coverage.

Christian Worstell is a senior Medicare and health insurance writer with MedicareAdvantage.com. He is also a licensed health insurance agent. Christian is well-known in the insurance industry for the thousands of educational articles he’s written, helping Americans better understand their health insurance and Medicare coverage.

..Christian Worstell is a senior Medicare and health insurance writer with MedicareAdvantage.com. He is also a licensed health insurance agent. Christian is well-known in the insurance industry for the thousands of educational articles he’s written, helping Americans better understand their health insurance and Medicare coverage.

Christian’s work as a Medicare expert has appeared in several top-tier and trade news outlets including Forbes, MarketWatch, WebMD and Yahoo! Finance.

Christian has written hundreds of articles for MedicareAvantage.com that teach Medicare beneficiaries the best practices for navigating Medicare. His articles are read by thousands of older Americans each month. By better understanding their health care coverage, readers may hopefully learn how to limit their out-of-pocket Medicare spending and access quality medical care.

Christian’s passion for his role stems from his desire to make a difference in the senior community. He strongly believes that the more beneficiaries know about their Medicare coverage, the better their overall health and wellness is as a result.

A current resident of Raleigh, Christian is a graduate of Shippensburg University with a bachelor’s degree in journalism.

If you’re a member of the media looking to connect with Christian, please don’t hesitate to email our public relations team at Mike@tzhealthmedia.com.

![]()

![]()

![]()

![]()

![]()

![]()

By clicking "Sign me up!” you are agreeing to receive emails from MedicareAdvantage.com.

Your Medicare guide will arrive in your email inbox shortly. You can also look forward to informative email updates about Medicare and Medicare Advantage.

If you'd like to speak with an agent right away, we're standing by for that as well. Give us a call!

LICENSED AGENTS AVAILABLE NOW