Medicare Supplement Insurance, also called Medigap, is a type of private insurance that is used together with your Original Medicare coverage (Medicare Part A and Part B) to help cover certain Medicare out-of-pocket expenses, such as copays and deductibles.

Medigap Plan A is one of the 10 Medigap plans available in most states, which include Plan A, B, C, D, F, G, K, L, M and N. Each type of Medigap plan offers a different combination of standardized benefits.

Let’s take a look at what Medicare Supplement Insurance Plan A covers and review the average cost of Medigap Plan A.

What does Medicare Supplement Plan A cost?

The average premium cost for Medicare Supplement Insurance Plan A in 2026 was $160.43 per month.1

It’s important to note that Medigap plan costs may vary based on factors such as age, gender, your health, how your insurance carrier rates (prices) its plans and where you live.

Medigap Plan A costs may also vary based on when you enroll.

The average cost listed above includes Medigap Plan A options that may offer lower premiums than what is listed, as well as some plans with higher premium costs.

What does Medicare Supplement Plan A cover?

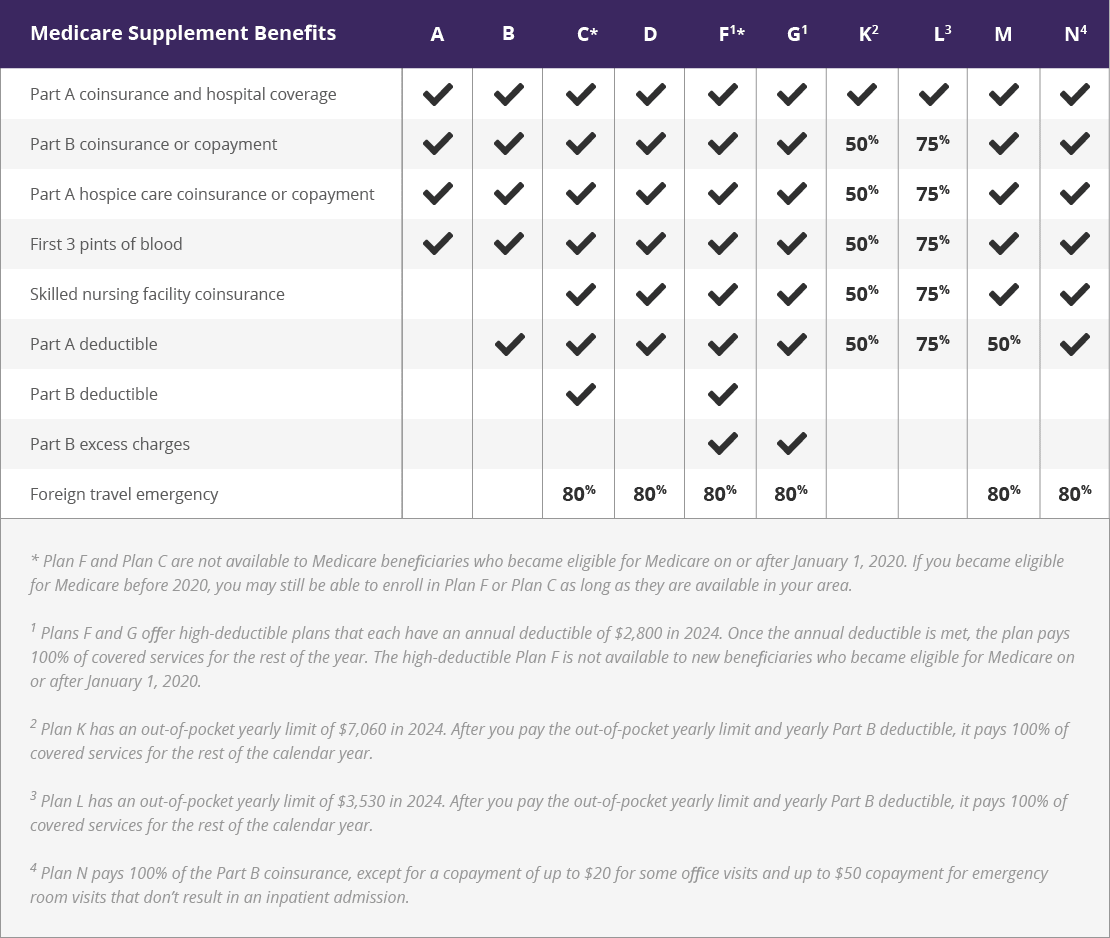

You can use the Medigap plans comparison chart below to compare Medigap Plan A benefits to what is covered by other Medigap plans.

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

|

|

|

|

|

|

|

|

|

|

| Part B coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A hospice care coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| First 3 pints of blood |

|

|

|

|

|

|

50% |

75% |

|

|

| Skilled nursing facility coinsurance |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A deductible |

|

|

|

|

|

|

50% |

75% |

50% |

|

| Part B deductible |

|

|

|

|

|

|

|

|

|

|

| Part B excess charges |

|

|

|

|

|

|

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

Medicare Supplement Insurance Plan A provides 100 percent coverage for each of the following four benefit areas:

Medicare Part A coinsurance and hospital costs

If you are admitted to a hospital for inpatient treatment, Medicare Part A helps cover your hospital costs once you reach your Medicare Part A deductible, which is $1,736 per benefit period in 2026.

For the first 60 days of your hospital stay, you aren’t required to pay any Part A coinsurance.

But beginning on day 61 of your stay, you’re required to make a Medicare Part A coinsurance payment of $434 per day through day 90. After your 90th day in the hospital, you must pay $868 per day for up to 60 more days. Beyond that, you are responsible for all costs.

These coinsurance costs can add up quickly. Medigap Plan A covers 100 percent of your Part A coinsurance costs.

Medicare Part B coinsurance or copayment

Medicare Part B helps cover costs for things like doctor’s appointments, medical devices and preventive care.

After you meet your Medicare Part B deductible (which is $283 per year in 2026), you are typically responsible for a coinsurance or copay of 20 percent of the Medicare-approved amount for covered services.

For example, if you suffer a foot injury and need to use a wheelchair, Part B will help cover 80 percent of the cost of your wheelchair (after you meet your Part B deductible).

For illustration purposes, if it costs $800 to buy the wheelchair and Medicare Part B covers it as durable medical equipment (DME), your Part B coinsurance cost would be $112. Medigap Plan A would fully cover your $112 Part B coinsurance.

First three pints of blood

Original Medicare does not cover the cost of the first three pints of blood you might need for a blood transfusion. Medicare Supplement Insurance Plan A covers 100 percent of the cost for your first three pints of blood.

Part A hospice care coinsurance or copayment

Medicare Part A requires a copayment for prescription drugs used during hospice care. You might also be charged a 5 percent coinsurance for inpatient respite care costs.

Medigap Plan A covers 100 percent of your Medicare Part A hospice care coinsurance or copayments.

What you need to know about Medigap Plan A

There are a few things to know about Medicare Supplement Insurance Plan A, beyond what it covers.

Medigap Plan A benefits are standardized

The basic benefits that are covered by Medigap Plan A are the same, no matter where the plan is sold, or by which carrier.

Medigap Plan A in Ohio offers the same basic benefits listed above as Medigap Plan A in Texas.

Medigap Plan A should not be confused with Medicare Part A

Medicare Supplement Insurance Plan A could sometimes be mistaken for Medicare Part A. But these are actually two very different things.

Medicare Part A is one part of Original Medicare (along with Medicare Part B). Medicare Part A provides coverage for hospital stays and other types of inpatient care.

Medigap Plan A helps cover some of the out-of-pocket Medicare costs listed above.

Medicare Supplement Insurance companies are required to sell Plan A

Any insurance company that sells Medicare Supplement Insurance plans must sell at least Medigap Plan A.

If they offer any additional Medigap plans, they are required to offer at least either Plan C or Plan F.

Medigap Plan A vs. Medicare Advantage plans

Medigap plans and Medicare Advantage plans are very different things. You cannot have a Medicare Supplement Insurance (Medigap) plan and a Medicare Advantage plan at the same time.

Medicare Advantage plans provide all the same benefits as Original Medicare. Medicare Advantage plans may also offer benefits that Original Medicare doesn’t cover.

Medicare Supplement Insurance does not offer any medical benefits or coverage for prescription drugs and other services. Medigap plans only cover certain Medicare Part A and Part B out-of-pocket costs as outlined above.

Medicare Supplement Insurance Plan A doesn’t cover everything

Medicare Supplement Insurance Plan A does not offer any coverage for the following Medicare costs:

Other Medicare Supplement Insurance plans may cover some or all of the benefits listed above, either partially or in full. Medicare Supplement Insurance Plan F, for example, covers all of them.

Learn More About Medicare Supplement Insurance

Medicare Supplement Insurance Plan A may or may not be right for your health care needs. Research all of the plans available where you live and speak with a licensed insurance agent to evaluate your needs.

Learn more about Medicare Supplement plans available where you live.

Speak with a licensed insurance agent

{kind=link}