57 percent of Original Medicare (Medicare Part A and Part B) beneficiaries are enrolled in a Medicare Supplement Insurance (Medigap) plan.1 These optional plans, issued by private insurance companies, help pay for some of the out-of-pocket costs that Original Medicare (Part A and Part B) doesn’t cover.

Plan F has long been the most popular Medigap plan. However, Medicare Supplement Plan F is no longer available for new Medicare beneficiaries. As a result, Plan G is quickly becoming the next most popular Medigap plan.

Let's explore the differences between Plan F vs. Plan G.

Compare plans today.

Speak with a licensed insurance agent

Did Medicare discontinue Plan F?

In April 2015, Congress passed the Medicare Access and CHIP Reauthorization Act to reduce some Medicare expenses. As part of that act, from January 1, 2020, insurers couldn't sell a policy that covers the annual Medicare Part B deductible to new Medicare beneficiaries.

This ruling effectively meant insurers couldn't offer Plan F or Medigap Plan C to people who became eligible for Medicare after January 1, 2020, because both plans cover the Part B deductible.

Beneficiaries who already had Plan F or Plan C before January 1, 2020 are able to keep their plan. If someone became eligible for Medicare before 2020, they can still apply for Plan F or Plan C if either plan is available where they live.

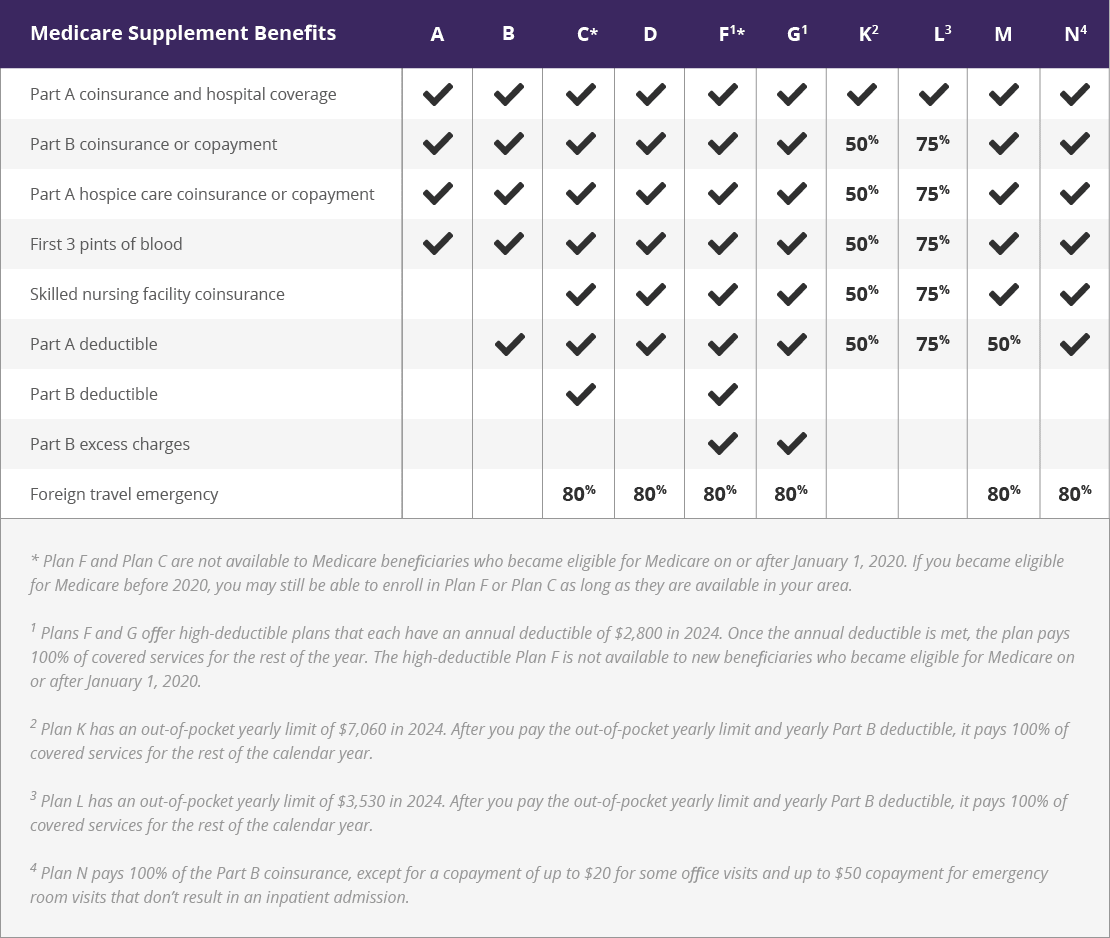

What are the similarities and differences between Medicare Plan F and Plan G?

If you're considering changing your Medigap insurance plan, understanding the similarities and differences between Plans F and G can help you make an informed purchasing decision.

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

|

|

|

|

|

|

|

|

|

|

| Part B coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A hospice care coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| First 3 pints of blood |

|

|

|

|

|

|

50% |

75% |

|

|

| Skilled nursing facility coinsurance |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A deductible |

|

|

|

|

|

|

50% |

75% |

50% |

|

| Part B deductible |

|

|

|

|

|

|

|

|

|

|

| Part B excess charges |

|

|

|

|

|

|

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

Benefits

Plan F and Plan G both provide 100% out-of-pocket coverage for:

- Medicare Part A coinsurance and hospital costs

- Medicare Part A deductible

- First three pints of blood used in a transfusion

- Skilled nursing facility coinsurance

- Medicare Part A hospice care coinsurance or copays

- Medicare Part B coinsurance or copays

- Medicare Part B excess charges

They also cover 80% of the costs of emergency care when traveling abroad. However, Plan F covers the Medicare Part B deductible while Plan G does not.

Policy premiums

Plan F and Plan G both charge monthly premiums. The cost of your monthly premiums depends on your Plan F or Plan G policy, and premiums may vary depending on where you live, the insurance company that offers your plan and the way the plan premium costs are rated.

Out-of-pocket limits

Plan F and Plan G have no limit on the qualifying out-of-pocket costs they'll absorb. That means you can incur high hospital costs after a severe injury, for example, and feel confident your Medigap plan will cover all those fees.

This knowledge can provide real peace of mind while you're getting back on your feet.

It’s important to note that Plan F and Plan G both do not include an annual out-of-pocket spending limit for you as a beneficiary. Because each plan offers coverage for most types of Medicare out-of-pocket costs, however, you are not likely to face high out-of-pocket Medicare costs if you have either plan.

Compare plans today.

Speak with a licensed insurance agent

High-deductible plans

High-deductible versions of Plan F and Plan G are available in some states. While the deductibles mean you must pay a certain amount of money out of pocket before the plan coverage kicks in, the monthly premiums are typically much lower than the premiums for other Medigap plans or for the standard non-deductible versions of Plan F and Plan G.

If you rarely use healthcare services, you might save money by paying the lower monthly premiums for a high-deductible plan.

Plan availability and premiums vary, so be sure to compare all of the Plan F or Plan G options that may be available where you live.

Availability

While new Plan F policies are no longer sold to new Medicare beneficiaries, existing policies still provide ongoing coverage in many states.

Residents in most states can purchase and use Plan G policies, though Massachusetts, Minnesota, and Wisconsin standardize their Medigap plans in different ways than most states.

Is Medicare Plan G better than Plan F?

As you can see, Medigap Plan F and Plan G are very similar. There are several points to consider when deciding which Medigap plan suits your need, especially if you already have Plan F coverage.

Plan F covers more than Plan G, as it includes the Medicare Plan B deductible. Plan F prices have also jumped substantially since the introduction of the act that discontinued their availability to new Medicare beneficiaries.

However, Plan G is also a comprehensive plan. The only benefit Plan F offers that Plan G doesn’t is coverage for the Medicare Part B deductible.

Even though Plan G doesn’t cover the Part B deductible, some Plan F options could have high enough premiums that the cost difference between Plan F vs. Plan G would be higher than the Part B deductible itself. If a Plan F option includes premiums that cost more in a year than the price of a Plan G policy plus the Medicare B deductible ($283 in 2026), then a beneficiary would save money by enrolling in Plan G.

Switching from Plan F to Plan G

If you enrolled in Plan F before 2020, you can continue your plan or switch to another Medigap plan, such as Plan G, if you prefer. You may want to make the change to reduce the price of your health insurance. However, every state has different rules worth considering before making the switch.

In some states, such as New York City, you can switch your Medigap plan at any time. There's a birthday rule in California that allows you to switch Medigap plans around your birthday. Both of these states may automatically approve any applications to switch plans, even if you have pre-existing health conditions.

In some other states, you may need to apply for a Plan G policy. If you apply during a time when you don’t have guaranteed issue rights, private insurance companies can use medical underwriting to determine your premium costs or to even deny you coverage altogether. In these states, sticking with your Plan F coverage may be your best Medigap option, or you may want to wait until you can switch to Plan G when you have guaranteed issue rights.

Compare plans today.

Speak with a licensed insurance agent

Medicare Supplement Plan F vs. Plan N

Medicare Supplement Plan F provides coverage for two areas that Plan N does not:

- Medicare Part B deductible

- Part B excess charges

Doctors who do not accept Medicare assignment reserve the right to charge up to 15 percent more than the Medicare-approved amount for services and items they provide. These costs are called excess charges.

Even though Plan N doesn't cover these excess charges, they are typically easy to avoid. Most doctors who accept Medicare patients also accept Medicare assignment, which means they accept the Medicare-approved amount as payment in full and won't charge any excess amounts. Be sure to ask your doctor if they accept Medicare assignment before receiving any treatment services.

Plan N typically has lower premiums than Plan F. In exchange for the lower monthly premiums, Plan N beneficiaries have to pay a copay of up to $20 for some doctor's office visits and a $50 copay for emergency room visits that don't result in being admitted for inpatient care.

Plan N can therefore be a good fit for beneficiaries who are looking for a plan with low monthly costs and who still want most of their Medicare out-of-pocket costs covered.

Choosing between Medicare Supplement Plan F vs. Plan G vs. Plan N

If you're ready to switch to Plan F, Plan G or Plan N, compare the plans available in your area to make sure you find the right Medigap plan for your health coverage needs.

Learn more about Medigap plans in your area

Speak with a licensed insurance agent

{kind=link}