Medicare Supplement Insurance, also called Medigap, is a type of private insurance that is used alongside your Original Medicare coverage (Medicare Part A and Part B) to help cover certain Medicare out-of-pocket expenses, such as copays and deductibles.

What was Medicare Plan J?

Medicare plan J was a medicare supplement plan that was designed to help for additional coverage that original medicare doesn't cover, such as copays from doctor visits, foreign travel benefits, preventive care, and some plans had prescription drug benefits as well.

Medigap Plan J was discontinued for new enrollees in 2010. Anyone who enrolled in Medicare Supplement Plan J prior to 2010 is allowed to keep the plan or they can sign up for a different type of medicare plan.

There are 10 Medigap plans that are currently available in most states, however. These plans include Plan A, B, C, D, F, G, K, L, M and N. Each type of Medigap plan offers a different combination of standardized benefits, which are outlined below.

Massachusetts, Minnesota and Wisconsin have different Medigap standards and plan options.

What do Medicare Supplement Plans cover?

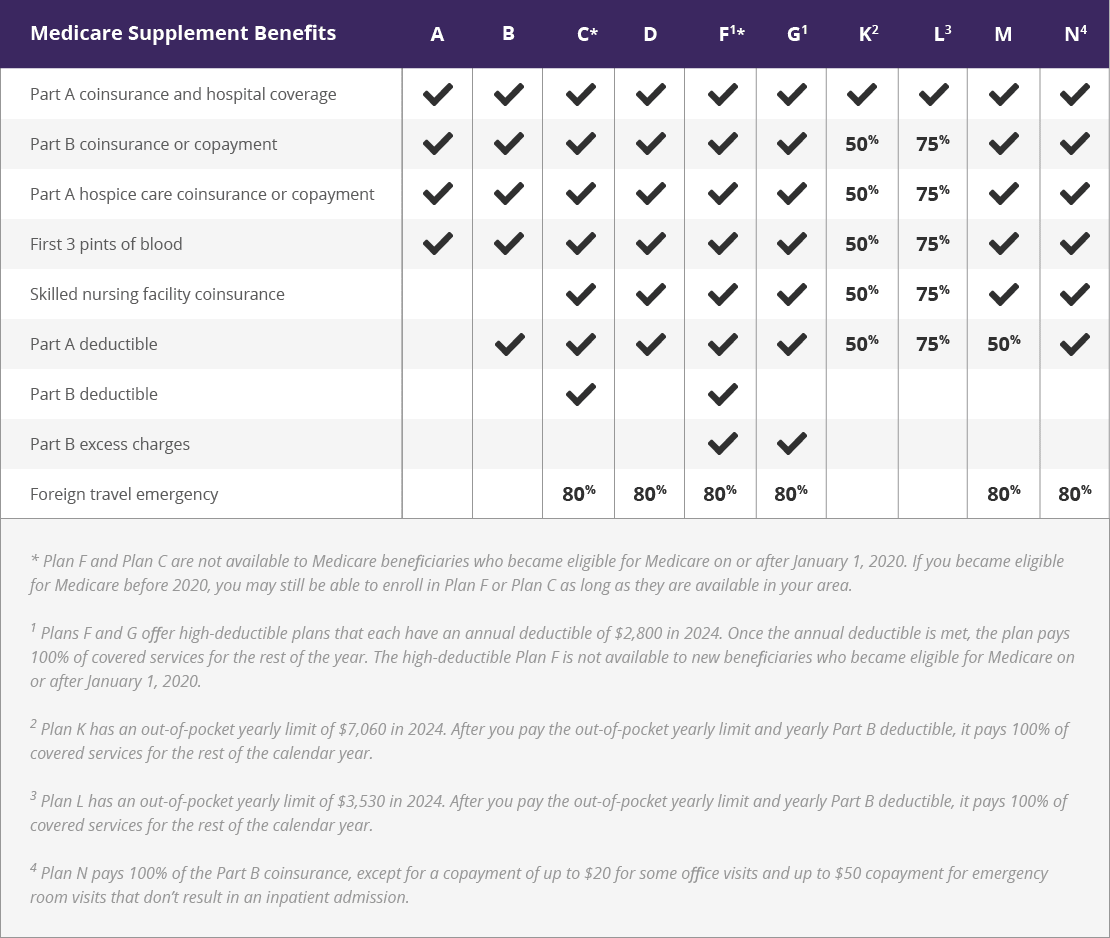

You can use the Medigap plans comparison chart below to compare the benefits of each type of Medicare Supplement Insurance plan that is still available for new enrollees in 2026.

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

|

|

|

|

|

|

|

|

|

|

| Part B coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A hospice care coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| First 3 pints of blood |

|

|

|

|

|

|

50% |

75% |

|

|

| Skilled nursing facility coinsurance |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A deductible |

|

|

|

|

|

|

50% |

75% |

50% |

|

| Part B deductible |

|

|

|

|

|

|

|

|

|

|

| Part B excess charges |

|

|

|

|

|

|

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

Why was Medicare Supplement Insurance Plan J discontinued?

Prior to 2003, Medicare did not offer retail prescription drug coverage (medications you’d get at your local pharmacy). At the time, certain Medigap plans – such as Medigap Plan J – covered prescription drugs for people who joined those plans.

But in 2003, Congress passed the Medicare Prescription Drug, Improvement and Modernization Act. This law introduced Medicare Part D plans, which are standalone Medicare prescription drug plans (PDP) sold by private insurance companies.

The 2003 legislation also expanded certain Original Medicare benefits. This included adding coverage for at-home recovery care and preventive care, which were previously covered by Medigap Plan J.

These additions – and later changes to Medicare in 2010 – made the benefits offered by Medicare Supplement Insurance Plan J redundant. Therefore, Medicare Supplement Insurance companies were no longer allowed to sell Medigap Plan J to new enrollees as of June 1, 2010.

Compare plans today.

Speak with a licensed insurance agent

What does Medicare Supplement Plan J cost?

The average premium cost for Medicare Supplement Insurance Plan J in 2025 was $154.75 per month.1

It’s important to note that Medigap plan costs may vary based on factors such as age, gender, health, how your insurance company rates (prices) its plans and where you live. The average cost listed above includes Medigap Plan J options that may have lower premiums than what is listed, as well as some plans with higher premium costs.

Remember, Plan J is no longer available for purchase for new enrollees.

Does Medicare Supplement Plan J cover prescriptions?

Medigap Plan J no longer covers prescription drugs. Medigap plans can only help cover certain out-of-pocket Medicare costs, such as deductibles and copayments.

If you want to get Medicare prescription drug coverage, you have two options:

- You can enroll in a Medicare Advantage Prescription Drug plan (MA-PD). These plans cover all of the same hospital and medical insurance benefits that are covered by Original Medicare.

- You can enroll in a standalone Medicare Part D Prescription Drug plan (PDP).

Please note that Medigap plans and Medicare Advantage plans are very different things. You cannot have a Medicare Supplement Insurance plan and a Medicare Advantage plan at the same time.

Compare plans today.

Speak with a licensed insurance agent

Should I switch from my Medigap Plan J to another Medigap plan?

As previously mentioned, beneficiaries who are currently enrolled in Medigap Plan J are allowed to remain in the plan. Only 2 percent of all Medigap beneficiaries are enrolled in Medicare Supplement Insurance Plan J.2

So if you currently have Plan J, should you keep it?

The first thing to consider is the plan cost. Because no new members are being accepted into Plan J, the overall plan risk pool can only increase in age and claim frequency. This may cause Plan J premiums to rise at a faster rate than other Medigap plan premiums.

The second factor to consider is benefits. While no other Medigap plan matches the coverage of Plan J, there are a few that come close. In fact, Plan F and Plan J are nearly identical.

Medigap Plan J vs. Plan F

The primary difference in benefits between Plan J and Plan F is the level of coverage offered for foreign emergency care.

Plan J covers 100 percent of the costs for qualified emergency medical care when you’re traveling abroad. Plan F covers 80 percent of foreign travel emergency care costs.

If you do a lot of traveling abroad, you might consider keeping your Plan J because of the more generous foreign emergency care benefit. But if you do not have plans to travel outside the U.S., the extra coverage for this benefit area may not serve much of a purpose for you.

Plan F is the second most popular Medigap plan currently available. 36 percent of all Medicare Supplement Insurance beneficiaries are enrolled in Plan F.2

Plan J vs. Plan G

Plan G offers all of the same benefits as Plan J, except – like Plan F – it only covers 80 percent of foreign travel emergency care costs. Plan G also does not cover the annual Medicare Part B deductible. (Medigap Plan F covers the Part B deductible).

The Medicare Part B deductible is $283 per year in 2026. If you can find a Plan G option that only costs $283 more per year (or less) than your current Plan J, you could save money in the long run by switching to Plan G (provided you don’t need the extra foreign emergency care coverage).

Plan J vs. Plan C

Another Medigap plan that closely matches Plan J is Plan C. Like Plan F and Plan G, Medigap Plan C covers 80 percent of foreign emergency care costs. Plan C also does not cover Medicare Part B excess charges. (Medigap Plan F does cover Part B excess charges).

Medicare excess charges are costs you may face if you receive medical services or items from a provider who does not accept Medicare assignment. This means that the provider does not accept Medicare reimbursement as full payment for their services.

These providers reserve the right to charge you up to 15 percent more than the Medicare-approved amount for your care.

You can avoid Medicare excess charges by visiting health care providers who accept Medicare assignment.

What happened to Medigap Plan C and Medigap Plan F in 2020?

Medicare Supplement Insurance Plan F offers more standardized benefits than the other current Medicare Supplement plans. Because of a new federal law, Plan F and Plan C aren't available for Medicare beneficiaries who became eligible on or after January 1, 2020.

If you already had Plan C or Plan F before 2020, you will be able to keep your plan. If you became eligible for Medicare before 2020, you may still be able to buy either Plan C or Plan F if either is available where you live.

Learn more about Medicare Supplement Insurance plans

While you can’t enroll in Plan J unless you currently have Plan J, there are several Medigap options that can provide you with nearly identical benefits. A licensed insurance agent can help you learn about plans in your area, what they cover and what they cost.

Learn more about Medicare Supplement plans available where you live.

Speak with a licensed insurance agent

{kind=link}