According to a 2020 study, people with traditional Medicare spend $5,801 on their insurance premiums and out-of-pocket medical expenses each year.1 One in 10 people with Medicare spends at least $10,268 out of their own pocket per year.

With so many people incurring such high costs each year, many turn to Medicare Supplement (also called Medigap) plans to fill their Medicare coverage gaps. One type of Medicare Supplement plan is a Medicare SELECT plan, which can feature monthly premiums that are typically lower than other types of Medicare Supplement plans.

What is a Medicare SELECT plan?

A Medicare SELECT plan is a type of Medicare Supplement Insurance policy sold by private insurance companies.

As with other Medigap policies, Medicare SELECT covers out-of-pocket expenses for Original Medicare beneficiaries. These policies are different from other types of Medigap plans, however, because they limit your coverage to a network of doctors, healthcare providers and hospitals, and if you go outside the network, you may not be covered.

Medicare SELECT plans aren’t available in every state.

What does Medicare SELECT cover?

Medicare SELECT plans may cover a percentage of out-of-pocket Medicare costs in the same way that the standard version of the plan would (for example, Medicare SELECT Plan G covers the same out-of-pocket Medicare costs as standard Medicare Supplement Plan G). The costs that Medicare SELECT plans can include expenses such as:

- The Medicare Part A deductible for inpatient care costs

- Coinsurance payments for Medicare Parts A and B

- Hospital costs for up to 365 days past your Part A coverage

- The first three pints of blood needed for a transfusion

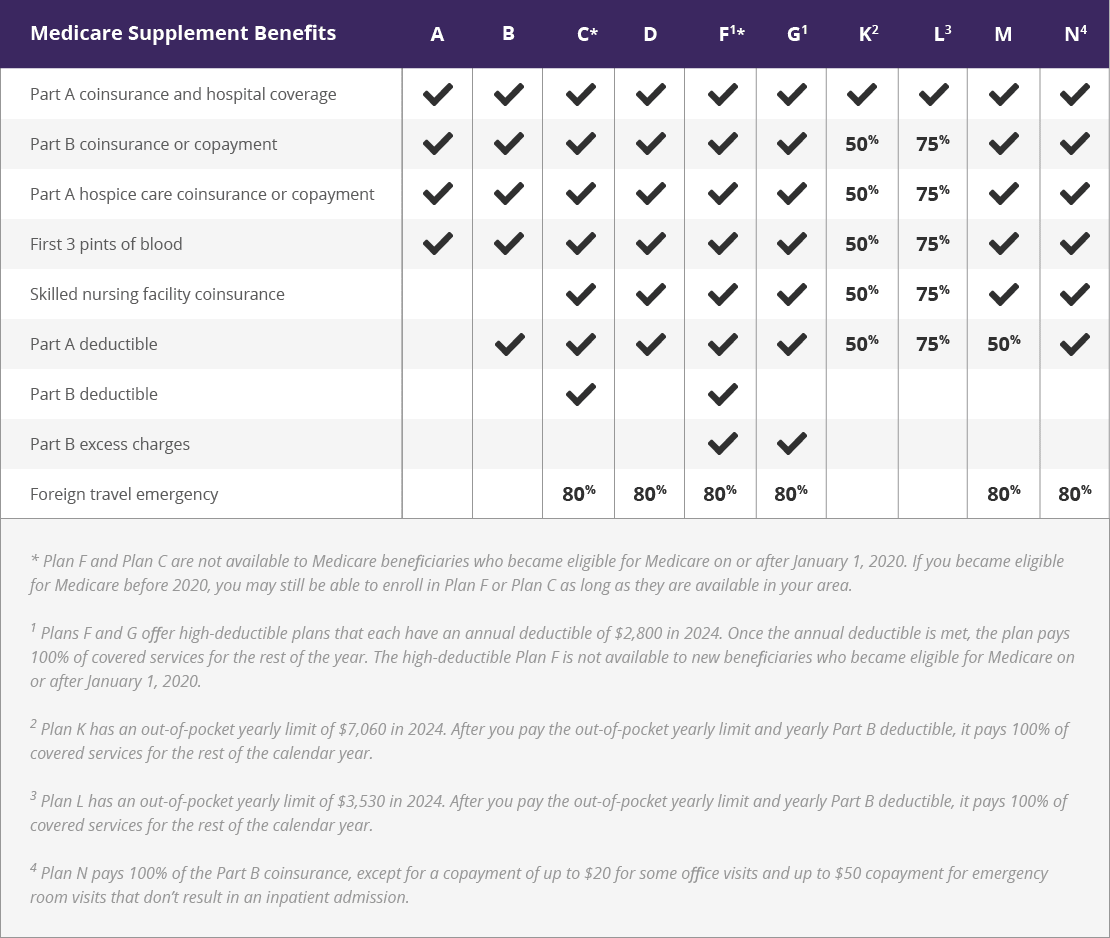

You can use the comparison chart below to view the costs that different types of Medigap plans cover side by side:

Click here to view enlarged chart Scroll to the right to continue reading the chart

Scroll for more

| Medicare Supplement Benefits |

A |

B |

C* |

D |

F1* |

G1 |

K2 |

L3 |

M |

N4 |

| Part A coinsurance and hospital coverage |

|

|

|

|

|

|

|

|

|

|

| Part B coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A hospice care coinsurance or copayment |

|

|

|

|

|

|

50% |

75% |

|

|

| First 3 pints of blood |

|

|

|

|

|

|

50% |

75% |

|

|

| Skilled nursing facility coinsurance |

|

|

|

|

|

|

50% |

75% |

|

|

| Part A deductible |

|

|

|

|

|

|

50% |

75% |

50% |

|

| Part B deductible |

|

|

|

|

|

|

|

|

|

|

| Part B excess charges |

|

|

|

|

|

|

|

|

|

|

| Foreign travel emergency |

|

|

80% |

80% |

80% |

80% |

|

|

80% |

80% |

What are the advantages and disadvantages of Medicare SELECT?

Medicare SELECT plans typically have much lower premiums than standard Medigap plans. That can make them an excellent choice for people who want to fill their Medicare coverage gaps while paying low monthly premiums for their Medigap plan.

However, these plans also have some rules and restrictions some people may find inconvenient. Plans only cover beneficiaries for medical care from providers in an approved network.

Except in emergencies, people with Medicare SELECT must use network providers or bear the full out-of-pocket costs when they receive care. Medicare SELECT beneficiaries also need a referral from their primary care doctor before receiving care at a hospital or specialist provider, except in medical emergencies.

It’s important to consider that restricted provider choice could affect your care. For example, imagine that someone has a heart condition, but the nearest hospital specializing in cardiothoracic surgery is outside the provider network. They would need to choose between getting the best care and paying all the out-of-pocket expenses or paying less to receive care at another less-than-ideal hospital.

Medicare SELECT plans are also not available in some areas of the country. The size of their network of providers also varies between locations and health insurance companies. While some areas may have many medical providers on their network, people living in other parts of the country may have fewer choices.

Is Medicare SELECT the same as Medicare Advantage?

While they are both available through private health insurance providers, Medicare SELECT plans and Medicare Advantage are two different health plans. Medicare SELECT complements your Original Medicare coverage. Conversely, Medicare Advantage plans replace Original Medicare by offering all of the same benefits and may offer benefits not found in Original Medicare as well.

You cannot have a Medicare SELECT and Medicare Advantage plan at the same time. It’s best to research and compare both options from a range of providers to decide which plan could work best for you.

How do I enroll in Medicare SELECT?

The process for applying for a Medicare SELECT plan is the same as enrolling in any other type of standardized Medicare Supplement plan.

The best time to apply for a Medicare SELECT plan is during your six-month Medigap open enrollment period, starts on the first of the month you are at least 65 years old and are enrolled in Medicare Part B. Applying during this open enrollment period guarantees coverage without answering any medical questions (known as medical underwriting).

You can apply for a plan at any time after this period, but if you apply when you don’t have a guaranteed issue right (such as during your Medigap open enrollment period), the insurance company will have the right to ask you some questions about your health. Depending on your answers, you may face higher premiums, restricted coverage or have your application denied altogether.

What if I decide Medicare SELECT isn’t for me?

If you enroll in a Medicare SELECT plan and decide you no longer want it, you can switch to any standard Medigap policy at any time within your first year of coverage. You might do this if you find the Medicare SELECT provider network too limiting, or you think a different plan may suit you better.

Switching your Medigap coverage during this period can help ensure you stay covered for your out-of-pocket Medicare expenses.

What if I move out of a Medicare SELECT coverage area?

If you have a Medicare SELECT plan and move to an area that’s no longer covered, you will most likely qualify for a guaranteed issue right and you’ll be able change to another Medigap policy.

Staying with your current health insurance provider means you may be able to easily switch to a Medigap policy with the same or fewer benefits. If you’ve been enrolled in Medicare SELECT for at least six months, you won’t need to answer any medical questions.

Alternatively, you can use your guaranteed issue right and switch to a new insurance provider’s Medigap Plan A, B, C, F, K, or L plan. These Medigap plans are available in most states, though they may not be available in all areas.

The benefits of Medicare SELECT

If you anticipate high out-of-pocket Medicare expenses or want to protect your budget against a shock from a medical bill, a Medicare SELECT plan may be an excellent option for you. While these plans have some restrictions, they often appeal to people on limited budgets or fixed incomes who don’t want a large monthly Medigap plan premium bill.

If you’re considering enrolling, remember that, as with all private health plans, Medicare SELECT policies vary. Compare several plans and their provider networks carefully to find the right one for your peace of mind.

Learn more about Medicare Supplement plans available where you live.

Speak with a licensed insurance agent

{kind=link}